![]()

Hundreds, and sometimes thousands, of shipping containers are lost at sea each year, resulting in significant financial losses for global shipping businesses. Lost containers can also present a collision risk for other vessels at sea, and depending on their contents, they could even lead to serious environmental damage.

In this post we will explore why so many shipping containers get lost at sea each year, and discuss how you can best protect your shipping business against financial loss.

How Many Shipping Containers Get Lost At Sea Every Year?

The World Shipping Council routinely surveys its member companies in order to estimate the number of shipping containers that get lost at sea each year.

The most recent survey, from 2025, covers the years up to and including 2024. Here are the total number of containers lost at sea over the past few years, according to World Shipping Council members:

- 2024 – 576

- 2023 – 221

- 2022 – 661

- 2021 – 2,301

- 2020 – 3,924

The World Shipping Council points out that over 250 million containers are shipped each year. 576 lost containers equate to just 0.0002% of this total. They also highlight how approximately 33% of all containers lost each year are ultimately recovered.

The World Shipping Council has been surveying their members in this way since 2011. Each year, they report a rolling three-year average. In the latest report, this stood at 489. In the previous report, the rolling three-year average was more than double this, at 1,061.

So, there is an encouraging downward trend. But the council also report a 10-year average of 1,274 containers lost each year. Every single lost container will lead to significant expenses, and each one poses a hazard to other vessels, and potentially to the environment too.

What Causes Shipping Container Loss?

Container falls

A container might fall from a vessel as a result of bad weather, collisions, or other incidents at sea. Human error can also play a part, should someone fail to correctly secure a container, for example. A ship may also choose to jettison its cargo in response to an onboard incident, such as a fire.

Global events

Global events can influence the total number of containers lost in a year. In recent years, unrest in the Middle East has forced many shipping routes to detour away from the Red Sea, and around the Cape of Good Hope.

Converging weather systems make extreme weather events, along with steep wave patterns, relatively common in this area. According to the South African Maritime Safety Authority, around 200 containers were recently lost around the Cape of Good Hope in the space of one year.

Isolated events

Occasionally, isolated events cause a major spike in the number of shipping containers lost in one year. 5,578 containers were lost in 2013, making this the worst year for losses in recent memory. This was largely due to a single incident in which an entire vessel was lost. Large scale incidents also occurred in 2020, when 3,924 containers were lost in a year, and 2021, which saw total losses of 2,301.

TopTier is an ongoing research project which is currently investigating these large scale losses in order to determine what went wrong, in the hope of identifying potential actions that could help prevent container loss.

Who is Liable For Shipping Container Loss?

Claims involving lost containers can get complicated. As well as the physical loss of the container, insurers must also consider any other containers that get damaged as a result of collapsing stacks, along with any damage the vessel itself sustains during the incident. Plus, as we mentioned above, a container lost at sea could ultimately damage other vessels, and could also have an environmental impact.

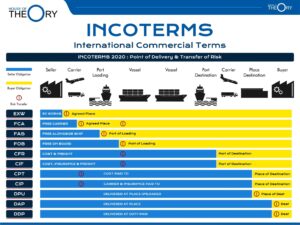

A shipping contract should outline who is responsible for costs and losses at each stage of the process. Whichever party is responsible for the goods during the passage at sea, whether that is the buyer or the seller, will have to ensure they are fully covered for potential container losses, along with the subsequent damages and costs that may arise.

Beyond this, the specific circumstances of the incident will determine who takes ownership of the container after it is lost. The cost of recovering lost containers, for instance, often falls on third parties. You can read our full guide to the different types of marine insurance loss claims.

Get Comprehensive Marine Insurance From James Hallam

Everard Insurance Brokers are the specialist marine trading division of James Hallam Limited who are accredited Lloyd’s brokers.

We can help you understand your liability concerning incidents of containers lost at sea, and we can help you ensure you have the dedicated insurance you need to cover you for all risks.