![]()

International commercial terms (incoterms) are a set of standard trade definitions that outline the specific responsibilities of buyers and sellers in international trade agreements. You can read our full guide to incoterms.

In this post we will take a closer look at two specific incoterms: DDP and DAP. We will explore the key differences between these two terms, and outline how they might affect your risks, responsibilities, and costs in an international shipping agreement.

DDP and DAP – A Brief Introduction

DDP (Delivered Duty Paid) and DAP (Delivered at Place) are both seller-focused incoterms. These terms apply to transactions where the seller, exporter, or manufacturer takes on most or all of the costs and risks associated with delivering goods to a named place of destination.

What is DDP in Shipping?

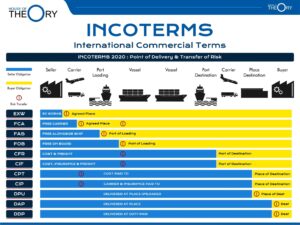

The DDP (Delivered Duty paid) incoterm places maximum responsibility on the seller.

Under a DDP contract, the seller, exporter, or manufacturer takes full responsibility for delivering goods to the agreed destination. They will cover all associated costs and risks, which includes all relevant customs and duties. Typically, the seller will include all of these expenses in the price of their goods, which can result in clear and transparent costs for all parties involved.

In a DDP arrangement, the buyer’s only responsibilities involve unloading the goods once they reach their destination. So, while the buyer will likely have to pay a higher price for the shipping, DDP remains a popular choice for buyers who are new to international shipping, and for those who want a frictionless and streamlined approach to entering new markets.

What is DAP in Shipping?

The DAP (Delivered at Place) incoterm is similar to the DDP incoterm, in that the seller is responsible for delivering goods to an agreed destination, covering all transport costs and bearing all risks until the goods reach their destination port.

The key difference between DAP and DDP is that, in a DAP arrangement, the seller does not take responsibility for covering any customs, taxes, and duties that may arise during the shipping process. Instead, the buyer will take responsibility for covering these costs. The seller generally will not include these charges in the total costs of their goods, meaning that the buyer will have less clarity and transparency when it comes to the total cost of the shipping.

However, the buyer will have full control over all import procedures, which often makes DAP the preferred arrangement for companies with pre-existing relationships with customs brokers, or for larger companies with established logistics expertise.

Is DDP or DAP Better For Sellers?

If you are a seller, you will have extensive responsibilities and liabilities regardless of whether you choose DDP or DAP. These will include:

- Preparing and packaging all goods for shipping.

- Arranging for shipping to the specified destination.

- Bearing all costs and all risks until the point the goods arrive at their destination – including all marine insurance costs.

- Providing all necessary documentation for customs and so on.

The only difference is that, with DDP, you will have to cover all customs, taxes, and duties on top of this.

If you would prefer an arrangement in which the buyer takes on more risks, or in which the buyer and the seller share the risks and the costs, read our complete guide to incoterms.

DDP or DAP – Which is Best For Buyers?

If you are a buyer, choose DDP if:

- You are inexperienced with international shipping, or you are looking to enter a new market, and you are happy for the seller to take care of everything.

- You want total clarity and transparency with the price you pay for shipping. In most cases, the price the seller quotes for shipping will include everything, including the costs of customs, taxes, duties, and insurance cover.

However, you might prefer DAP if:

- You want flexibility with your transport options. DAP arrangements are compatible with all forms of transport, including air, rail, road, and sea.

- You have established relationships with customs brokers, or you have in-house logistics expertise, so you would prefer to handle all customs, duties, and tax procedures yourself.

One more thing to consider: Choosing either DDP or DAP will tie you to your seller’s price structure and supply chain. For one reason or another, this might not suit your needs. Alternative incoterm arrangements would give you greater flexibility, but most would require you to take on additional costs, risks, and liabilities.

For more information, read our full guide to incoterms.

How DDP and DAP Affect Insurance in Shipping

The incoterms you use during your transactions will determine the level of insurance cover you need, whether you are the buyer or the seller.

In both DDP and DAP transactions, the seller takes on the most risk. The responsibilities only transfer from the seller to the buyer at the point of delivery, at which point the buyer is responsible for ensuring all goods are safely unloaded.

Whichever code you use, and whichever party you are in the transaction, it is essential that your insurance covers you for all the risks and responsibilities as outlined in your contract.

Everard Insurance Brokers are the specialist marine trading division of accredited Lloyd’s brokers James Hallam Limited. We can help you understand the cost, risk, and insurance implications of any incoterm you use, and we can help you get the specialist cover you need at a competitive price.

Find out more about our dedicated marine insurance services, or call us on 020 3148 9540 or email info@everardinsurance.co.uk.